_web.webp?t=1781766065)

Refinance surge kept lenders hopping

Golf Savings hired more than 100 employees, though swell might now ebb

A home-mortgage refinancing surge that began in December has caused banks and credit unions here to scramble to meet demand from consumers who want to take advantage of historically low interest rates, though there are signs now that the surge could be ending.

Some institutions have seen record volume of loan applications, and hired additional staff to handle the several-month-long swell. Last week, however, rates began to edge up after the Fed's moves to keep them down began to lose their effect.

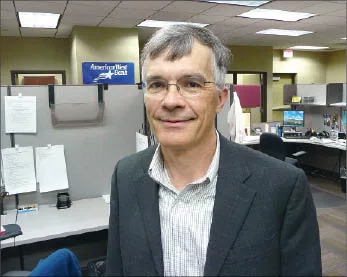

"The environment is fun, exciting, scary, and tough—all of the above," says Mike Koch, senior vice president and director of residential lending at Spokane-based AmericanWest Bank, which in the past four months has seen the highest volume of mortgage lending in its history.

To meet a surge in loan activity, Golf Savings Bank, the mortgage lending subsidiary of Spokane-based Sterling Financial Corp., hired 100 new employees during the first three months of this year, says Donn Costa, an executive vice president at the bank.

Last November, Golf tallied its worst loan origination month in two and a half years, with $80 million in originations. In December, after mortgage rates fell, that number jumped to $400 million, and so far this year the bank has averaged $550 million a month in originations, Costa says.

"We were at a real low point in November, looking to reduce staff," he says.

That changed quickly. With the 100 new employees, Golf now employs about 500 people, Costa says.

Spokane Teachers Credit Union also saw record volume, says Don Frigaard, director of real estate at the Spokane credit union. During the first quarter of this year, STCU funded 400 mortgages worth a total of more than $68 million, compared with 306 loans for $51 million during the first quarter of 2008. The year-earlier volume also was a record for the credit union, Frigaard says.

STCU likely will average about $27 million in monthly volume in April and May, which would be double the volume of those months in 2008. More than 90 percent of STCU's home-mortgage volume is from refinancing, Frigaard says.

At Wells Fargo Home Mortgage's office in Coeur d'Alene, loan originations have been running three times as high as they were in the fourth quarter, says area manager Jeff Grutta. Such originations now are the highest they've been since 2003, he says.

"It came on really quickly," says Grutta, who adds that 80 percent of the office's current volume is from refinancing.

Enticing rates

Mortgage rates began dipping in December after the Federal Reserve announced plans to buy $500 billion of mortgage-backed securities issued by Fannie Mae, Freddie Mac, and Ginnie Mae, which have ties to the government, plus $100 billion in direct obligations from Fannie, Freddie, and the Federal Home Loan Banks. The announcement boosted confidence in mortgage-backed securities, which are sold to raise capital for mortgages.

At that time, interest rates for 30-year fixed-rate mortgages fell to under 5 percent, and they generally stayed roughly at that level until last week.

On May 29, last Friday, interest rates shot up to 5.44 percent on 30-year fixed-rate mortgages, the highest point in months. Freddie Mac said fixed-rate mortgage rates climbed in response to higher long-term bond yields, which typically influence the cost of home loans.

Koch says rates essentially have been kept artificially low by the government's purchases of mortgage-backed securities, and that those continued purchases aren't sustainable in the long term.

"There's upward pressure because of that," he said. "We're going to see rates trend upward."

Contacted before rates climbed last week, Wells Fargo's Grutta said, "No one knows for sure how long it (low interest rates) will last," but that if a home owner or prospective buyer were "waiting for a specific target interest rate, that might make them miss the boat."

After rates had climbed some late last week, a Wells Fargo spokesman said the higher rates still compare well to the 6.08 percent rate seen a year ago.

To keep up with the volumes seen this year, Wells Fargo hired four additional mortgage consultants and an additional support staff person in Coeur d'Alene, Grutta says.

STCU, meanwhile, has hired three new people for its mortgage operations since December, Frigaard says, and also has been using temporary employees to meet the higher demand.

The credit union has gone from being an average-size mortgage lender in the Spokane area to one of the top lenders, Frigaard says. Last year, the credit union closed mortgage loans totaling $152 million, compared with $92 million in 2007 and $68 million in 2006. Already this year, it has closed loans worth $120 million, he says.

At Golf, the 100 additional staff members have helped the Sterling unit keep loan applications moving through the system briskly, typically closing loans in 30 to 60 days, Costa says.

About 65 percent of its volume is from refinancings, while the rest is new loans for homes. In some of the markets it serves, however, those percentages are flipped, particularly where home values have fallen enough that home owners can't take advantage of the low refinancing rates because they don't have enough equity in their homes.

Different this time

Those in the industry say the recent refinancing boom differed somewhat from earlier booms in that most home owners now are simply trying to lower their house payment and boost cash flow, rather than pulling equity out of their homes to pay off other debt or to make purchases.

Others are trying to get out from under other types of loans, such as adjustable-rate loans that proved to be too volatile in recent years, observers say.

"People are wanting to get positioned for the future in a fixed rate," says Wells Fargo's Grutta. "Some in fixed mortgages want to go to a different term" than they had before.

Adjustable-rate mortgages (ARMs) have fallen out of favor, he says, though he adds that Wells Fargo still offers such loans.

"By far, the majority are taking fixed-rate products," Grutta says. "It just makes sense right now."

Meanwhile, a minority of home owners are pulling out equity during the rush to refinance, bankers say.

"In the past, more than 50 percent were taking some equity out in the transaction," Grutta says. "In this particular refinance rally, less than 50 percent are taking cash."

There has been a change of focus, he says. "That is: cash in as opposed to cash out."

So when is it a good time to refinance?

STCU's Frigaard says that depends on the amount of the loan, how much the interest rate would change from the home owner's current loan rate, and closing costs. Home owners also must consider how long they would remain in their home, which determines whether they would be able to recoup the closing costs with savings from a lower monthly payment.

Grutta says a refinance should lower a home owner's mortgage payment enough so that the monthly savings covers their closing costs within 18 months. After that, the monthly savings should all be net gain, he says.

Although refinancing currently makes up the majority of home-mortgage activity, there is demand for loans to purchase a home.

Costa says that although first-time home buyers don't make up the majority of that latter group, loans to first-time buyers are a larger share of Golf's volume than normal, with enticing interest rates available, coupled with incentives intended to attract first-time buyers into the market. Under the federal stimulus package, first-time home buyers might qualify for a tax credit of up to $8,000.

Says AmericanWest's Koch, "It's a buyer's market today. This is a good time for them, because sellers are likely to be motivated to assist."

Other changes

Golf Savings' Costa says recent changes in the world of banking and lending also have changed the mortgage industry.

"At the end of the day, the changes will make the market stronger," Costa says. "It's really, really healthy."

One such change has been how institutions view what the industry refers to as stated-income loans, he says. Stated-income loans refer to the practice of borrowers inflating their income to get a loan and lenders accepting those artificial numbers to keep the borrower from going to another institution.

"Stated-income loans and no-income loans are gone," Costa says.

Now, lenders are more diligent about getting full documentation for each loan, and detailing the borrower's true income and assets, he says.

"That's as it should be; it benefits both the borrower and bank," Costa says.

Another important recent change was the activation of the Home Valuation Code of Conduct, which became effective May 1 and is intended to enhance the independence and accuracy of the appraisal process and to provide added protections for home buyers, mortgage investors, and the housing market.

One important aspect of the code, says Costa, is that it keeps loan officers from selecting the appraiser involved in evaluating property before a loan, which prevents the appraiser from feeling the need to push values upward or to face the possibility of getting less appraisal work from lenders.

"It's fraud prevention," Costa says. "It keeps appraisers from feeling pressure to push values" to stay busy and retain the business of lending institutions.

"It keeps them from thinking, 'I'm not going to get another deal if I don't push it,'" he says.

_web.webp?t=1782975679)

_web.webp?t=1781766165)