Preparers here advise clients to plan for big tax changes

Businesses, individuals urged to strategize to reduce exposure to hikes

Tax professionals here are urging their clients to forge tax strategies now for changes ahead.

The health-care legislation Congress is busy working on now likely will be funded in part by higher tax rates on individuals and businesses in upper income brackets, says Chris Hesse, director of taxation for the Spokane-based accounting firm, LeMaster Daniels PLLC.

One of Congress' first orders of business following health-care reform will be to address estate taxes, Hesse says.

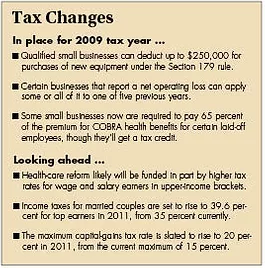

A 45 percent tax now applies to estates valued at more than $3.5 million. The federal tax will expire in 2010, if Congress doesn't act. Then, the tax is scheduled to return with rates starting at 41 percent on estates valued at more than $1 million.

Hesse says he believes Congress will extend the estate tax into 2010 and later raise the exemption that's currently scheduled to go into effect in 2011.

"Tax professionals and contacts I know say there will be a bill before the end of the year or a couple of months into 2010 that will fix the estate tax," he says. "I don't believe Congress is going to allow people to die in 2010 without an estate tax."

A host of other tweaks likely will be made to estate-tax legislation, Hesse says, although he declines to speculate on what they might be.

"When there's necessary legislation, there's also a lot of riders," he says.

When it comes to personal income taxes next year, the Obama administration is likely to push the president's campaign pledge that no family making less than $250,000 a year will see an income-tax increase, Hesse says.

If Congress does nothing, the Bush tax cuts will expire, and the tax rate for the highest income bracket for married couples filing jointly will return to 39.6 percent in 2011, up from 35 percent now, he says. Also, the top tax rate on capital gains will rise to 20 percent in 2011, up from 15 percent.

Hesse says the administration likely would have to tweak income-tax and capital gains-tax rates for some brackets to fulfill Obama's campaign promises, although Congress isn't likely to take action on that this year.

"It doesn't need to happen until before the end of 2010," he says.

Meantime, people whose income hasn't increased during the recession in 2009 might see a tax cut of sorts through the increases in personal-exemption deductions and the standard deduction that were implemented this year.

Each personal exemption is worth a $3,650 deduction in taxable income, up from $3,500 in 2008. For 2009, the standard deduction for married couples filing jointly rises to $11,400, up from $10,900 in 2008.

When it comes to stock holdings, some clients are having to deal with issues of worthless stock rather than capital gains, says David Green, a tax partner at the Spokane office of Seattle-based Moss Adams LLP.

Worthless stocks have to be claimed as such in the year that they become worthless, and the IRS requires documentation of "facts and circumstances" by those who claim the loss, Green says.

He's advising clients of a simpler way to claim a loss on worthless stocks.

"Instead of trying to determine when a stock went worthless, ask the broker to buy it for a penny or so," Green says. "That completes a transaction at a known date, because you have a sale. It's a stronger case to have a sale to report rather than claim something as worthless."

Green says he also is advising clients to perform year-end tax projections now.

"It's an opportunity to know what the return will look like," he says. "People in upper-income brackets need to know where they stand before they do tax planning."

Green says he recently met with a client who had underpaid taxes because he hadn't had enough income withheld from his paychecks.

"He's got five paychecks left to bump withholding and avoid paying fees and penalties to the IRS," Green says.

If tax projections show a client is subject to the alternative minimum tax, planning is different than if a client is subject to regular taxes, he says.

To reduce tax liability, business owners can buy more equipment and shelter it under the Section 179 expense deduction, which was nearly doubled to $250,000 for 2009. In some cases, the section 179 expensed deduction can be combined with another provision that allows accelerated depreciation of 50 percent of the cost of new equipment beyond $250,000, he says.

Andrew McDirmid, a partner at the Spokane-based accounting firm McDirmid, Mikkelsen & Secrest PS, says the recession has prevented most small businesses from taking advantage of the Section 179 provisions.

"With the general tightening of credit, it's harder for small businesses to decide to spend money," McDirmid says.

Also, business owners are worried tax rates are going to climb, and they're putting off spending that might be deductible under higher tax rates later.

Under another stimulus-bill provision, certain clients who run businesses that incur net operating losses this year have to decide whether to carry the losses forward to subsequent years or to take advantage of the loss carry-back option, which allows them to apply losses in one of five prior years, Green says.

The loss carry-back provision provides a degree of certainty in that it would reduce a past tax liability and trigger a refund, he says.

"If, however, I had a client that had a bad year in 2009, and I knew 2010 and 2011 would be great years, and with tax rates likely to increase, I would carry it forward," Green says.

McDirmid says one stimulus-package provision certain business owners should be careful not to overlook is a new rule requiring small businesses to provide 65 percent of the premium coverage for Consolidated Omnibus Budget Act (COBRA) health benefits for nine months for qualifying former employees laid off from Sept. 1, 2008, to Dec. 31, 2009.

The employer's share of the premium can be recovered in the form of a tax credit by subtracting it from the payroll tax payment, he says.

McDirmid says his firm has filed several amended 2008 tax returns due to the first-time homebuyer provision of the stimulus bill that allows a tax credit of up to $8,000 for qualified buyers. The provision allows qualified taxpayers who bought homes in 2009 to claim the credit on their 2008 taxes to "get their hands on the money much sooner," he says.

Green says some owners of C corporations should start or review 10- to 15-year tax plans now. "With the economy being in the doldrums, now is a great time to minimize values and to look at long-term planning," he says.

Green advises owners of C corporations to check into whether it would be advantageous to convert to S corporations. Converting to an S corporation would shift income-tax liability to shareholders and away from the corporation, he says.

Any business owner who is planning on selling a company or passing it on to another generation within 10 to 15 years likely would prefer an S corporation, Green says.

_web.webp?t=1785394978)